The 50/30/20 Budget Rule: Complete Guide for Beginners

Managing money effectively is one of the most important skills for achieving financial stability and long-term wealth. Yet many people struggle to create a budget that is both simple and sustainable. Fortunately, the 50/30/20 budget rule offers an easy-to-follow framework that can help anyone take control of their finances.

Popularized by U.S. Senator and bankruptcy expert Elizabeth Warren in her book All Your Worth: The Ultimate Lifetime Money Plan, the 50/30/20 rule divides your after-tax income into three categories: needs, wants, and savings. This budgeting strategy is widely recommended because it is flexible, easy to understand, and suitable for beginners.

Whether your goal is to save more money, pay off debt, build an emergency fund, or achieve financial freedom, this complete guide explains everything you need to know about the 50/30/20 budget rule and how to make it work for your lifestyle.

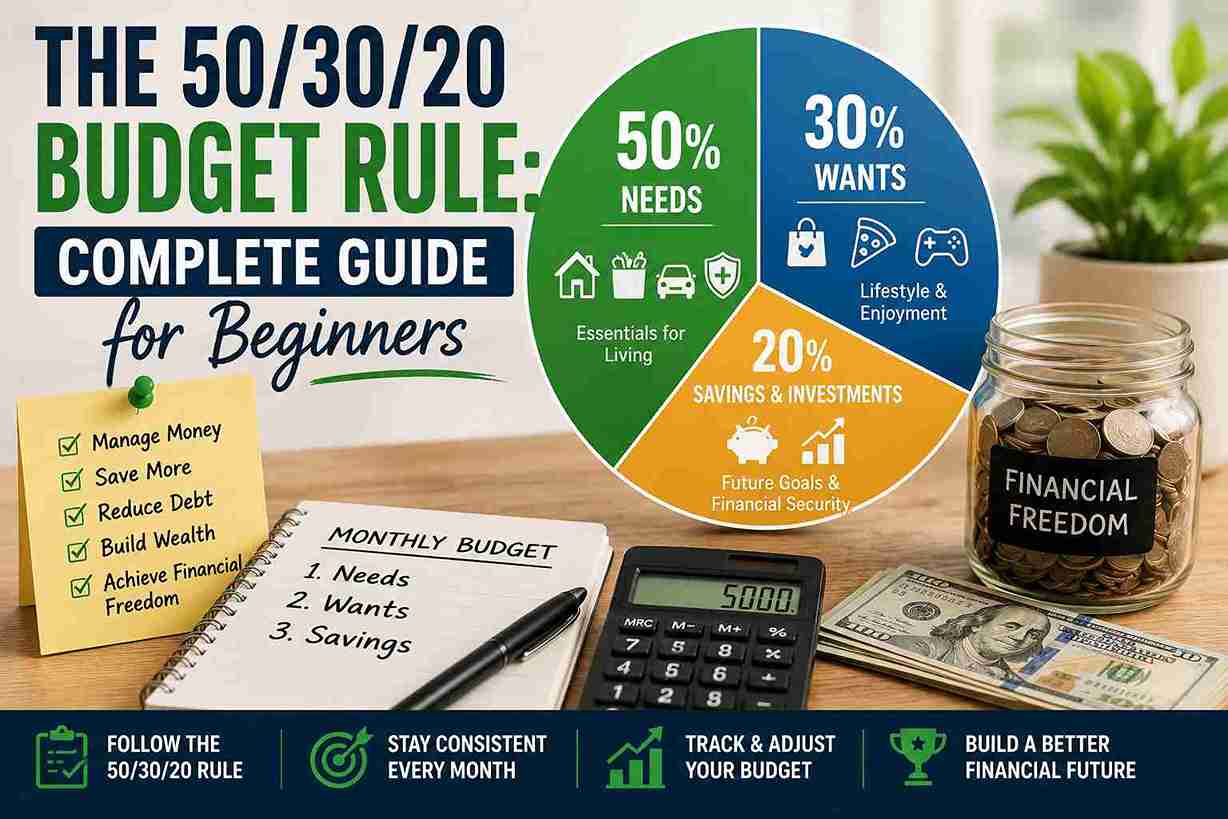

What Is the 50/30/20 Budget Rule?

The 50/30/20 budget rule is a simple budgeting method that divides your monthly after-tax income into three spending categories:

- 50% for Needs

- 30% for Wants

- 20% for Savings and Debt Repayment

Instead of tracking hundreds of spending categories, this system simplifies financial planning by focusing on three broad areas.

For example, if your monthly take-home income is $4,000, your budget would look like this:

| Category | Percentage | Monthly Amount |

|---|---|---|

| Needs | 50% | $2,000 |

| Wants | 30% | $1,200 |

| Savings & Investments | 20% | $800 |

This balanced approach helps ensure that your essential expenses are covered while still allowing room for enjoyment and future financial growth.

Why the 50/30/20 Budget Rule Works

One reason this budgeting strategy remains popular is its simplicity.

Unlike complicated budgeting systems, the 50/30/20 rule doesn’t require tracking every dollar spent.

Its benefits include:

- Easy for beginners

- Flexible for different income levels

- Encourages healthy spending habits

- Promotes consistent saving

- Helps reduce financial stress

- Supports long-term wealth building

Because it balances today’s needs with tomorrow’s goals, many financial planners recommend it as a starting point for personal finance.

Understanding the 50% Category: Needs

Needs are the expenses required to maintain your basic standard of living.

Without these essentials, it would be difficult to live or work.

Examples include:

- Rent or mortgage payments

- Property taxes

- Utility bills

- Groceries

- Health insurance

- Transportation costs

- Fuel

- Internet required for work

- Minimum debt payments

- Childcare expenses

- Essential medical costs

These expenses should ideally remain within 50% of your monthly after-tax income.

How to Reduce Your Needs

If your essential expenses exceed 50%, consider:

- Refinancing loans

- Moving to a lower-cost home

- Using public transportation

- Comparing insurance providers

- Reducing utility usage

- Meal planning to lower grocery costs

Lowering fixed expenses creates more room for saving and investing.

Understanding the 30% Category: Wants

Wants include expenses that improve your lifestyle but are not essential for survival.

Examples include:

- Dining out

- Entertainment

- Streaming subscriptions

- Vacations

- Shopping

- Designer clothing

- Gym memberships

- Hobbies

- Coffee shop visits

- Upgraded electronics

These purchases make life enjoyable, but they should not interfere with your financial goals.

How to Control Spending on Wants

If you consistently overspend, try these strategies:

- Follow a shopping list.

- Wait 24 hours before making large purchases.

- Cancel unused subscriptions.

- Limit impulse buying.

- Set monthly spending limits.

Reducing discretionary spending often leads to significant long-term savings.

Understanding the 20% Category: Savings and Investments

The final 20% is the most important category for building wealth.

This portion of your income should be used to strengthen your financial future.

Examples include:

- Emergency fund contributions

- Retirement savings

- Stock market investing

- Index funds

- Mutual funds

- Exchange-Traded Funds (ETFs)

- Paying extra toward high-interest debt

- Saving for a home

- College savings

- Building passive income

Consistently saving and investing this 20% can dramatically improve your long-term financial health.

How to Create a 50/30/20 Budget

Creating your budget is straightforward.

Step 1: Calculate Your After-Tax Income

Use your monthly take-home pay after taxes and payroll deductions.

For freelancers or business owners, calculate your average monthly income after taxes.

Step 2: List Your Monthly Expenses

Review bank statements and categorize every expense.

Separate them into:

- Needs

- Wants

- Savings

This exercise often reveals spending patterns you may not have noticed.

Step 3: Compare Your Current Spending

Determine whether your spending aligns with the recommended percentages.

If not, identify areas where adjustments can be made.

Step 4: Set Spending Limits

Assign maximum monthly amounts for each category.

Using the earlier example of $4,000 monthly income:

- Needs: $2,000

- Wants: $1,200

- Savings: $800

These limits create structure without being overly restrictive.

Step 5: Track Your Progress

Review your budget at the end of each month.

Adjust as necessary while staying focused on your long-term financial goals.

Example of a Monthly 50/30/20 Budget

Suppose your monthly after-tax income is $5,000.

Needs (50%)

- Rent: $1,300

- Utilities: $250

- Groceries: $500

- Transportation: $300

- Insurance: $150

Total: $2,500

Wants (30%)

- Restaurants: $250

- Entertainment: $200

- Shopping: $300

- Travel savings: $400

- Streaming services: $100

- Hobbies: $250

Total: $1,500

Savings & Investments (20%)

- Emergency fund: $300

- Retirement account: $300

- Index fund investment: $250

- Extra debt payment: $150

Total: $1,000

This balanced allocation supports both current living and future wealth.

Advantages of the 50/30/20 Budget Rule

The popularity of this budgeting method comes from its practicality.

Benefits include:

Simplicity

Easy to understand and implement.

Financial Balance

Encourages responsible spending while allowing enjoyment.

Consistent Saving

Builds wealth through regular investments.

Debt Reduction

Supports faster repayment of high-interest debt.

Less Financial Stress

Provides a clear financial roadmap.

Potential Drawbacks

Although effective, the 50/30/20 rule may not suit everyone.

Possible limitations include:

- High housing costs in expensive cities

- Low-income households may spend more than 50% on essentials

- Self-employed individuals with fluctuating income may need greater flexibility

- Large families may have higher essential expenses

If necessary, adjust the percentages while maintaining the principle of prioritizing savings.

Tips to Make the 50/30/20 Rule More Effective

To maximize results:

- Automate savings transfers.

- Increase your income through a side hustle.

- Review subscriptions regularly.

- Meal prep to reduce food costs.

- Avoid lifestyle inflation after salary increases.

- Invest consistently every month.

- Build an emergency fund before making riskier investments.

- Track expenses using budgeting apps.

Small improvements can produce significant financial benefits over time.

Common Budgeting Mistakes to Avoid

Avoid these mistakes:

- Not tracking expenses

- Ignoring small purchases

- Overspending on discretionary items

- Failing to adjust your budget as income changes

- Skipping emergency savings

- Using credit cards to finance lifestyle spending

- Giving up after one difficult month

Budgeting is a long-term habit, not a one-time exercise.

Frequently Asked Questions

Is the 50/30/20 Budget Rule Good for Beginners?

Yes. Its simplicity makes it one of the best budgeting methods for people who are new to personal finance.

Should Debt Payments Count Toward the 20%?

Minimum loan payments are generally considered “Needs.” Extra payments made to eliminate debt faster can be included in the 20% category.

Can I Change the Percentages?

Absolutely.

For example:

- 60/20/20

- 50/20/30

- 40/30/30

The ideal budget depends on your income, cost of living, and financial goals.

Is the 50/30/20 Rule Suitable for High-Income Earners?

Yes.

Many high-income earners use this framework but often increase the percentage allocated to savings and investments to accelerate wealth building.

Final Thoughts

The 50/30/20 budget rule is one of the easiest and most effective ways to manage your money. By dividing your income into needs, wants, and savings, you create a balanced financial plan that supports both your current lifestyle and your future goals.

Remember that budgeting is not about restricting your life—it is about making intentional decisions with your money. Whether you’re paying off debt, building an emergency fund, investing for retirement, or saving for a major purchase, this budgeting method provides a practical roadmap toward financial success.

Start today by calculating your after-tax income, categorizing your expenses, and applying the 50/30/20 rule. With consistency and discipline, you’ll develop healthier financial habits, reduce stress, and move steadily toward financial freedom.

SEO Keywords Included

50/30/20 budget rule, budgeting for beginners, personal finance, monthly budget, budgeting tips, money management, financial planning, save money, budgeting method, emergency fund, financial freedom, wealth building, debt repayment, investing, after-tax income, savings goals, budgeting strategy, financial literacy, smart spending, household budget.